Audit & Assurance

Audit & Assurance

Posted on 7th August 2024

Download PDF

With the increasing focus on environmental, social and governance (ESG) issues, mandatory climate disclosure reporting is being introduced around the world to provide information on an organisation’s progress towards their ESG goals. To demonstrate their commitment to acting on climate change in their own operations, the Commonwealth Government has introduced Climate Disclosure Reporting for Commonwealth entities and Commonwealth companies.

Like the introduction of Performance Statements into Commonwealth Government reporting, the introduction of Climate Disclosure Reporting will be applied in a phased approach to allow entities to develop their maturity over time. However, do not let this phased approach lull you into a sense of false security, for entities and Accountable Authorities to properly discharge their responsibilities under Climate Disclosure Reporting entities must invest in the relevant resources and take the time to develop and implement the appropriate infrastructure to support this reporting.

There will be two streams of disclosure requirements for Commonwealth entities and

Commonwealth companies:

The Department of Finance expect to finalise the Commonwealth Climate Disclosure requirements for Stream 2 in mid-2024. Therefore at the time this paper was written, only the requirements for the Pilot had been released. However, the Department of Finance notes that the requirements will align with climate disclosure standards set internationally by the International Sustainability Standards Board (ISSB), nationally by the Australian Accounting Standards Board (AASB), and be tailored for government and the regulatory and policy environments under which they operate (e.g. APS Net Zero by 2030).

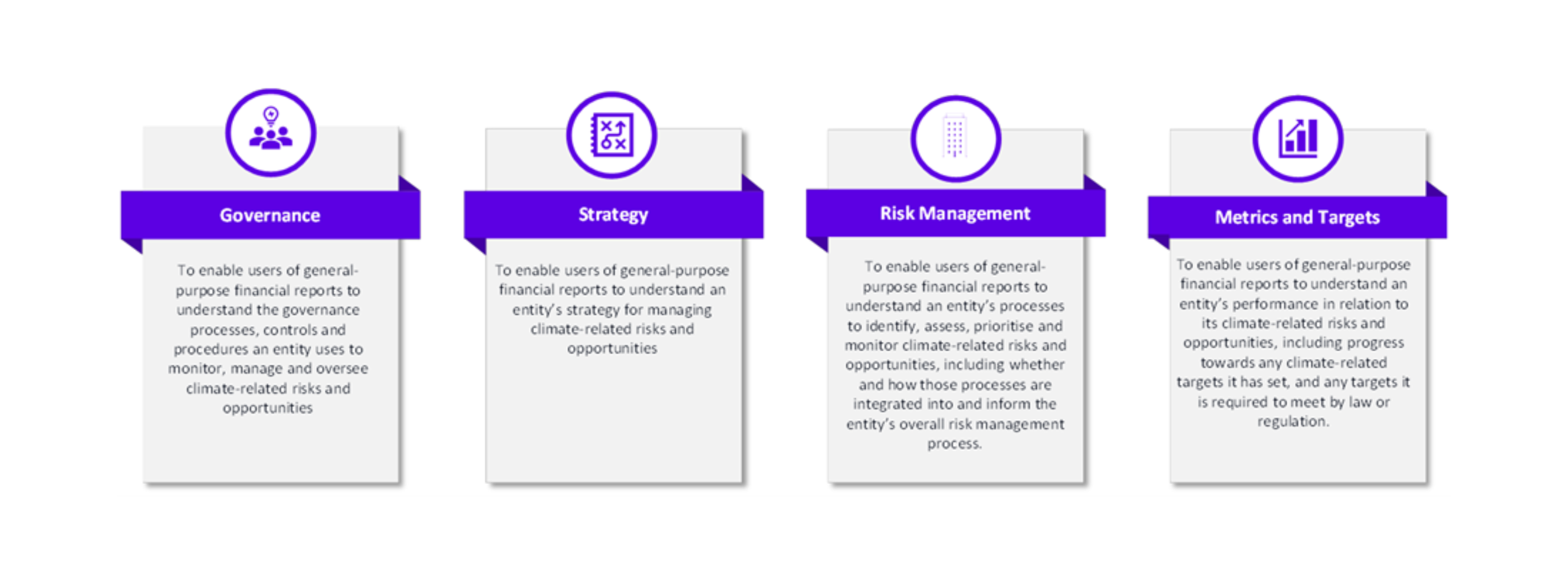

The pillars of Climate Disclosure reporting within International Financial Reporting Standards Sustainability Standard S2 Climate-related Disclosures that will be featured within the Department of Finance’s disclosure requirements include:

It is noted that the pillar of ‘Strategy’ is not included in the Pilot for Departments of State, however this pillar will be included in the required disclosures by the Department of Finance from 2024-25.

Similar to the introduction of Performance Statements and the new Australian Accounting Standards for Revenue and Leases, entities that are not aware of their requirements and adequately prepare for climate disclosure reporting will get caught out in the first year of reporting.

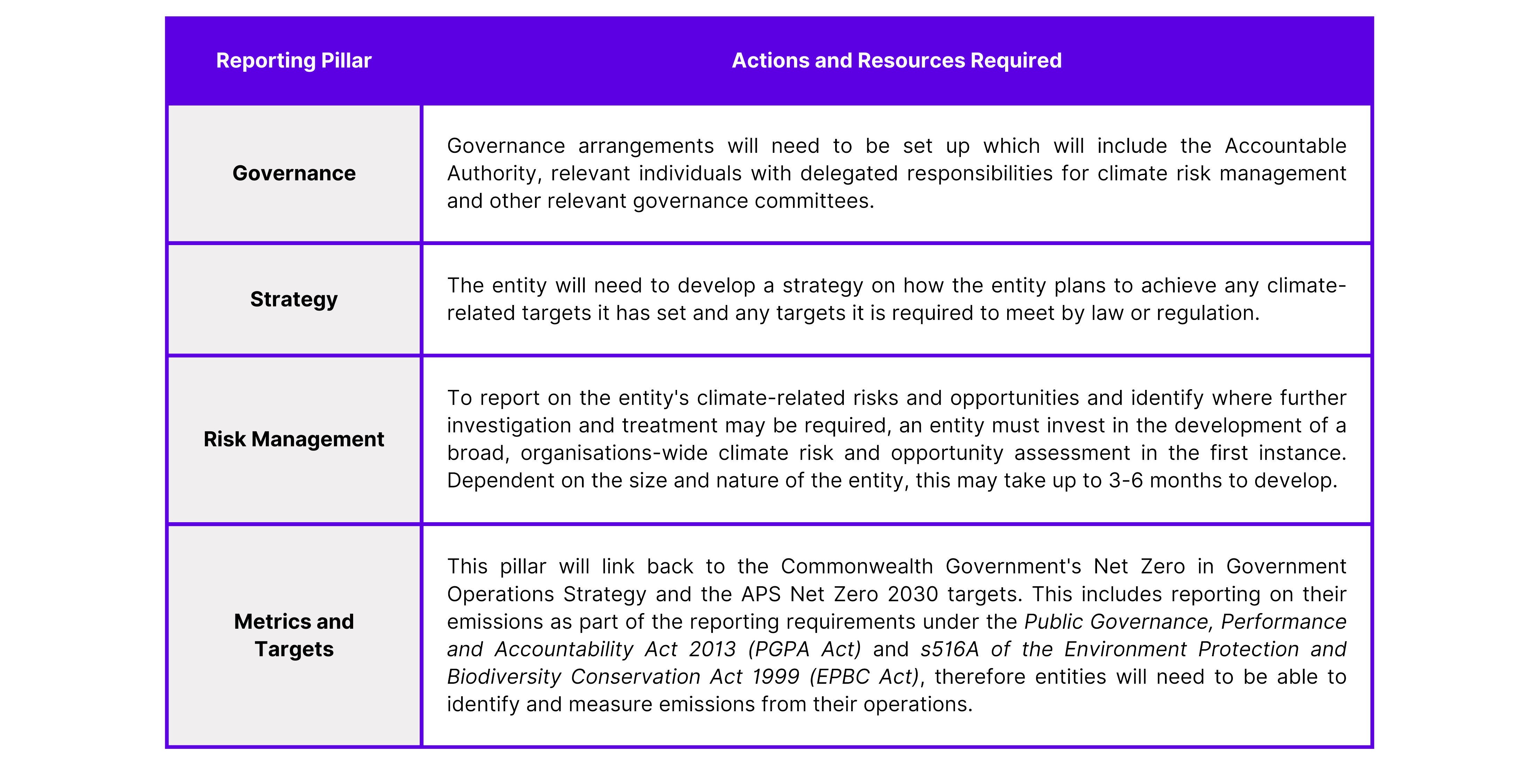

For an entity, and therefore an Accountable Authority, to properly discharge their responsibilities under Climate Disclosure Reporting, an entity must take the time to ensure that they have the right resources and infrastructure in place. To report on the four pillars, this will include:

Although capacity building support is being provided to Commonwealth entities and Commonwealth companies to help them meet their climate disclosure obligations, entities need to ensure that they have dedicated resources with the capability and experience to be able to properly report on their climate disclosure requirements. In addition, employee engagement and staff led initiatives will be important to achieving net zero grassroots climate action and broader sustainability. Dependent on the size and nature of the entity, to ensure that there is the appropriate infrastructure, frameworks and level of executive involvement, this may require the establishment of a Chief Sustainability Officer, a Climate Sustainability and Assessment Team, a Risk Management Team and an Environmental Contact Officer Network (a volunteer-run network of staff committed to reducing the environmental footprint of the entity’s operations).

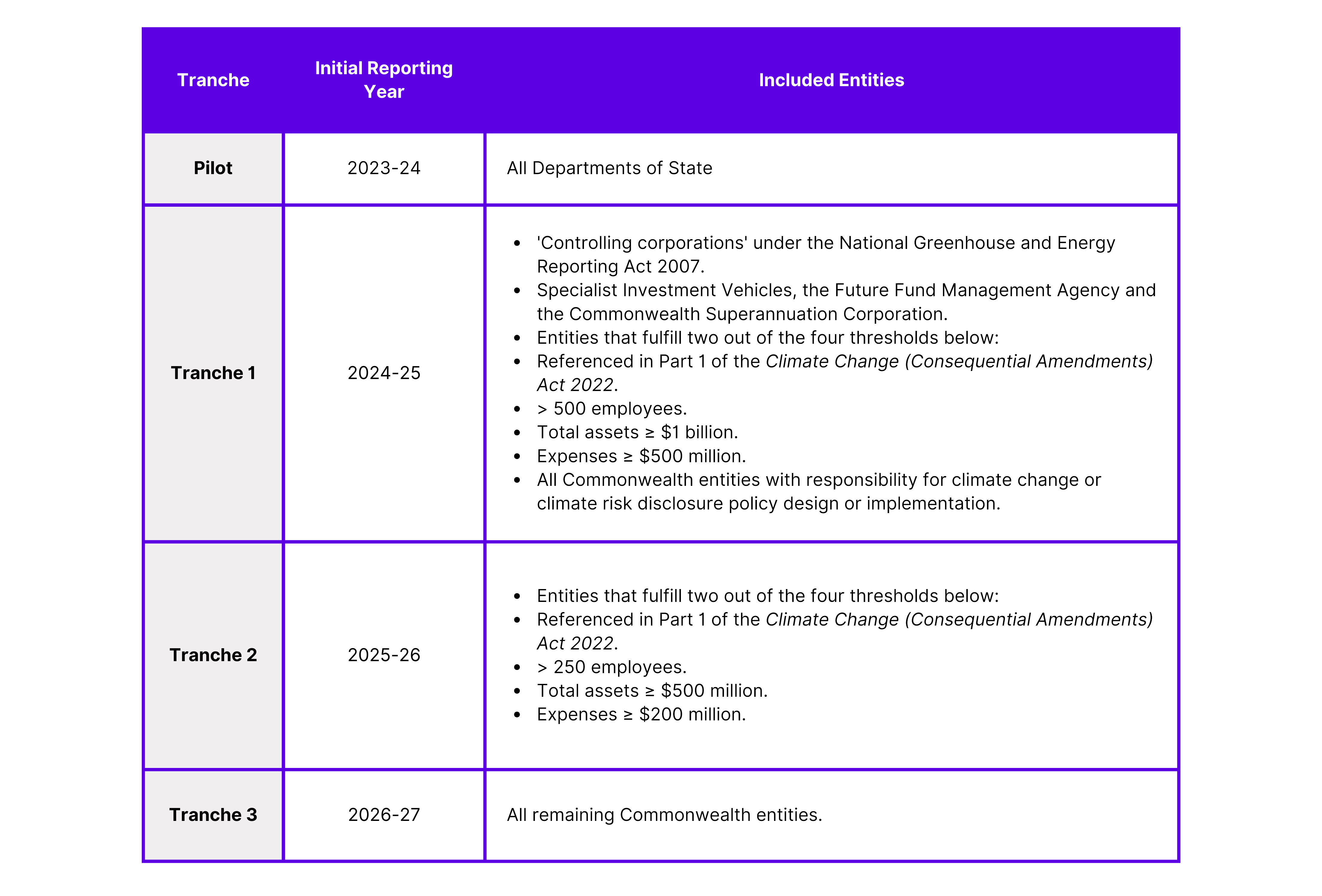

The following table details the tranche and initial year of reporting for all Commonwealth entities under Stream 2:

The Department of Finance will be developing a verification and assurance regime in consultation with the Australian National Audit Office (ANAO) to be applied to Stream 2 entities. Like the initial Performance Statement reviews conducted by the ANAO, the focus of the regime will be on improving the quality of climate disclosures. We believe that over the years as the maturity of climate disclosure reporting increases within the Commonwealth, like the Performance Statements there may be a move to mandatory audits which will include the issue of an audit opinion in the form of positive assurance over compliance with the Commonwealth climate disclosure reporting requirements. With this in mind, entities should develop their climate disclosure reporting frameworks to ensure that there is rigor and robustness within processes to identify and capture applicable data, and ensure that the governance around this function supports the complete and accurate reporting of the climate disclosure requirements of the entity. This will also provide the Accountable Authority with comfort over what the entity is reporting as well as their progress in line with the Commonwealth Government’s commitment to Net Zero in Government operations.

Internal Audit should play a significant part in an entity’s preparedness for Climate Disclosure Reporting, and now is the perfect time for Internal Audit to get involved! Internal Audit should be making contact with the line areas responsible for Climate Disclosure Reporting and integrating into an assurance program over the four pillars of reporting. Real time assurance as the entity progresses around the framework for Climate Disclosure Reporting, as well as assurance over results to be reported, will provide relevant governance committees and the Accountable Authority comfort in what the entity is reporting to both government and the public.

Conversely, line areas responsible for Climate Disclosure Reporting should be reaching out to Internal Audit to provide them assurance around the rigor and robustness of their processes for Climate Disclosure Reporting.

Our team of big thinkers will work closely with you to deeply understand your challenges and create lasting impact. For us that means building capability, doing work that's part of something bigger, and reflecting the best of what consulting can be to uplift organisations and the communities they serve.